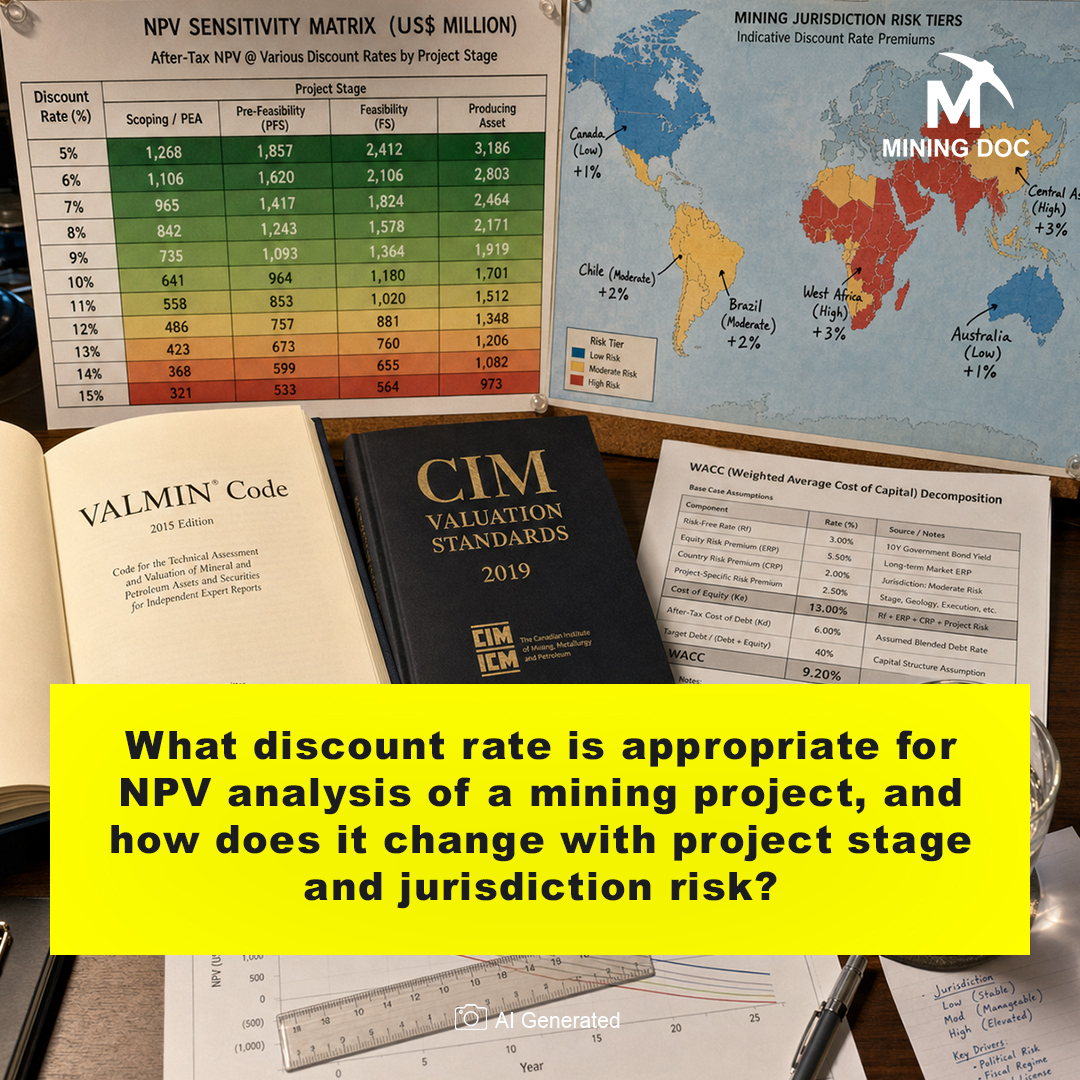

Net Present Value, or NPV, is a key tool for judging if an investment could be profitable. It finds the difference between how much cash comes in and goes out, adjusted to what that money is worth right now, over the project’s expected life. Since a dollar today is worth more than one promised in the future, we use something called a discount rate to adjust those future cash flows. For the mining industry, this rate covers both how much the money’s worth today and the dangers seen in the project. If there’s a lot of risk, they need a higher rate to make the investment worthwhile (Ovalle, 2020).

The determination of the right baseline discount rate requires careful financial modeling. Usually, professionals use the Weighted Average Cost of Capital (WACC) or the Capital Asset Pricing Model (CAPM) to set this base rate. Both models figure the expected return by mixing a risk-free rate, like long-term government bonds, with a market risk premium tailored to the asset’s specific risk level. Plus, the CAPM is often highlighted as a great framework for setting the basic cost of capital in resource extraction industries, according to Komzolov et al., 2021.

The discount rate for a mining project isn’t fixed; it changes depending on how far along the project is. When mining begins with exploration and scoping, there’s tons of uncertainty; both technically and geologically. During these early phases, the evaluation can be quite subjective. Companies look mainly at the potential of the geological features, and because the risks are so high at this point, the discount rates usually are in the double digits to cover the possibility of failure.

But when an exploration makes it through to definitive feasibility and production starts, the risks start to fall. This progression allows more detailed and reliable studies, which help in understanding what resources are really there and what the real costs will be. By the time a mine is fully up and running with known reserves and steady income, the risks, and therefore the discount rates, are way lower. If we go by the numbers, once mining projects reach this mature phase, the typical discount rate settles somewhere between 7% and 8.5% (Ovalle, 2020).

Beyond technical maturity, jurisdiction risk really stands out as a key factor affecting the final discount rate. Typically, a Country Risk Premium (CRP) is added to the base rate to cover the political, legal, and economic instability of the host country. So, mining projects in jurisdictions known for resource nationalism, shaky tax systems, or civil unrest need a higher expected return. These high-risk projects have to jump through more financial hoops to be considered viable, using a bumped-up discount rate to account for those specific risks (Davis et al., 2024).

In the end, the determination of the right discount rate for a mining project’s NPV analysis involves combining broad economic guidelines with the project’s particular challenges. This requires balancing statistical models like the CAPM with practical adjustments based on the asset’s technical life cycle and the local geopolitical scene (Komzolov et al., 2021). Adjusting the discount rate as risks decrease over time and adding penalties for political uncertainty helps analysts calculate a realistic NPV. This way, they get a clear picture of how economically feasible their project truly is.

References

Davis, G. A., Bou Habib, C., Solheim, G., & Lokanc, M. (2024). Maximizing Output and Government Revenues from Mining in Developing Countries: The Role of Country Political Risk and Investors’ Return, and Implications for the Energy Transition. Washington, DC: World Bank. https://doi.org/10.1596/1813-9450-10965

Komzolov, A., Kirichenko, T., Kirichenko, O., Nazarova, Y., & Shcherbakova, N. (2021). The Problem of Determining Discount Rate for Integrated Investment Projects in the Oil and Gas Industry. Mathematics, 9(24), 3327. https://doi.org/10.3390/math9243327

Ovalle, A. (2020). Analysis of the discount rate for mining projects. MassMin 2020: Proceedings of the Eighth International Conference & Exhibition on Mass Mining, 1048–1064. https://doi.org/10.36487/acg_repo/2063_76