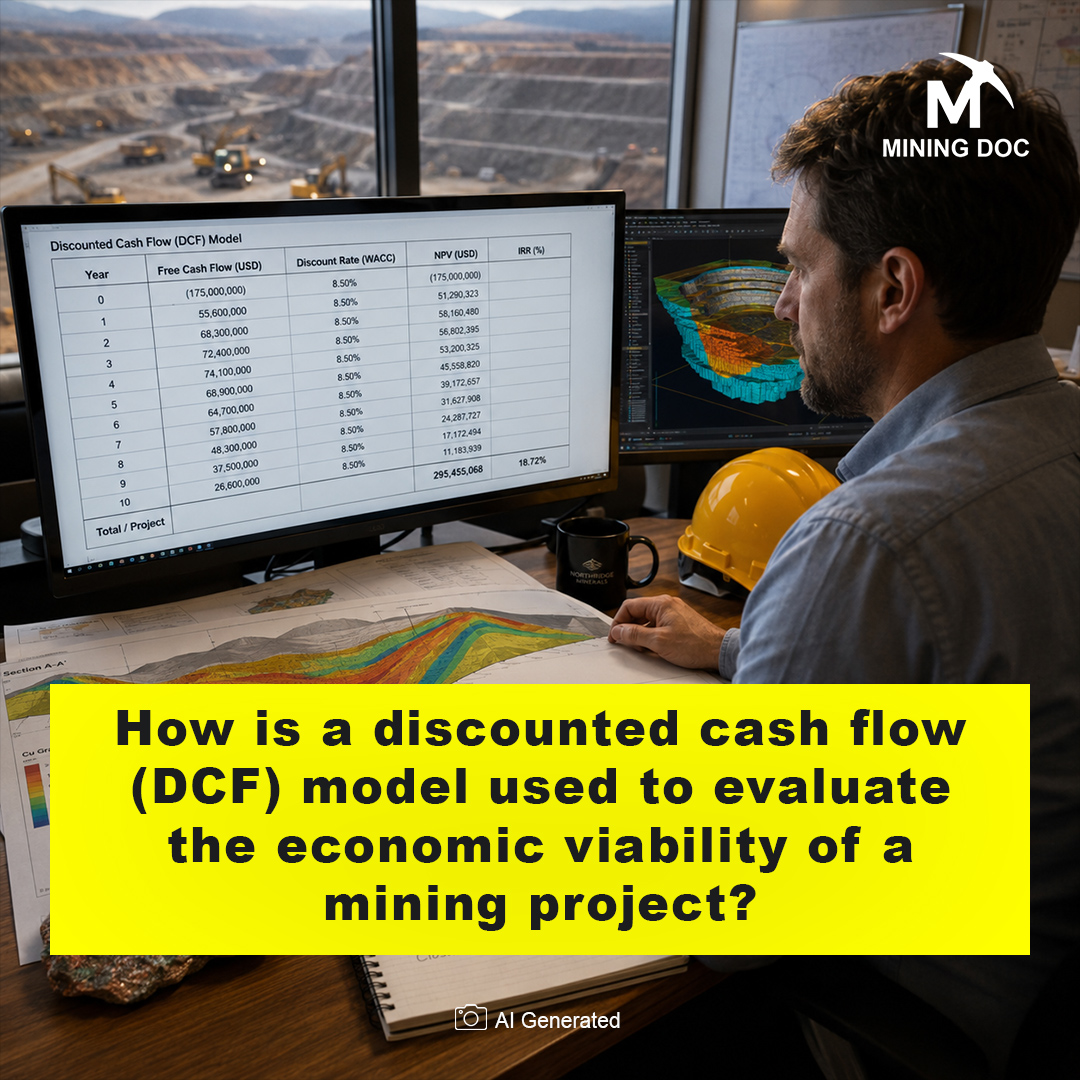

The Discounted Cash Flow model is a way of valuing an investment based on its estimated future cash flows and the calculation of their present value through an appropriate discount rate considering the time value of money. In scientific sources, such as publications in mining economics, the DCF approach is referred to as the present value of expected cash flows (or flow-to-equity), calculated according to models such as the capital asset pricing model (CAPM).

In mining operations, DCF assesses economic feasibility by projecting cash flow throughout the project’s lifetime, starting from discovery to mine closure, with geological uncertainties and commodity price fluctuations included. In its calculations, it uses specific life-of-mine (LOM) plans developed during feasibility studies that estimate revenue generation from the sale of minerals against operational costs such as extraction and rehabilitation costs.

The fundamental data used in DCF are expected net cash flows: revenues (volume × grade × recovery × metal prices) less operating costs (OPEX), capital costs (CAPEX), taxes, royalties, and working capital. The initial CAPEX occurs at t=0, whereas sustaining CAPEX and closure costs come after; thus, precise ore reserves are necessary.

The discount factor incorporates the time value of money, risk factors such as political, technical risks, and opportunity costs. The rate used for mining projects ranges from 5 to 10 percent when carrying out feasibility studies while 15 percent and above for risky businesses.

A positive NPV implies that the project is valuable, while the IRR measures the project’s return relative to other options. The sensitivity analysis examines the impact of factors such as price and cost, whereas the Monte Carlo simulation deals with uncertainties, thus improving the DCF method in the highly risky mining sector.