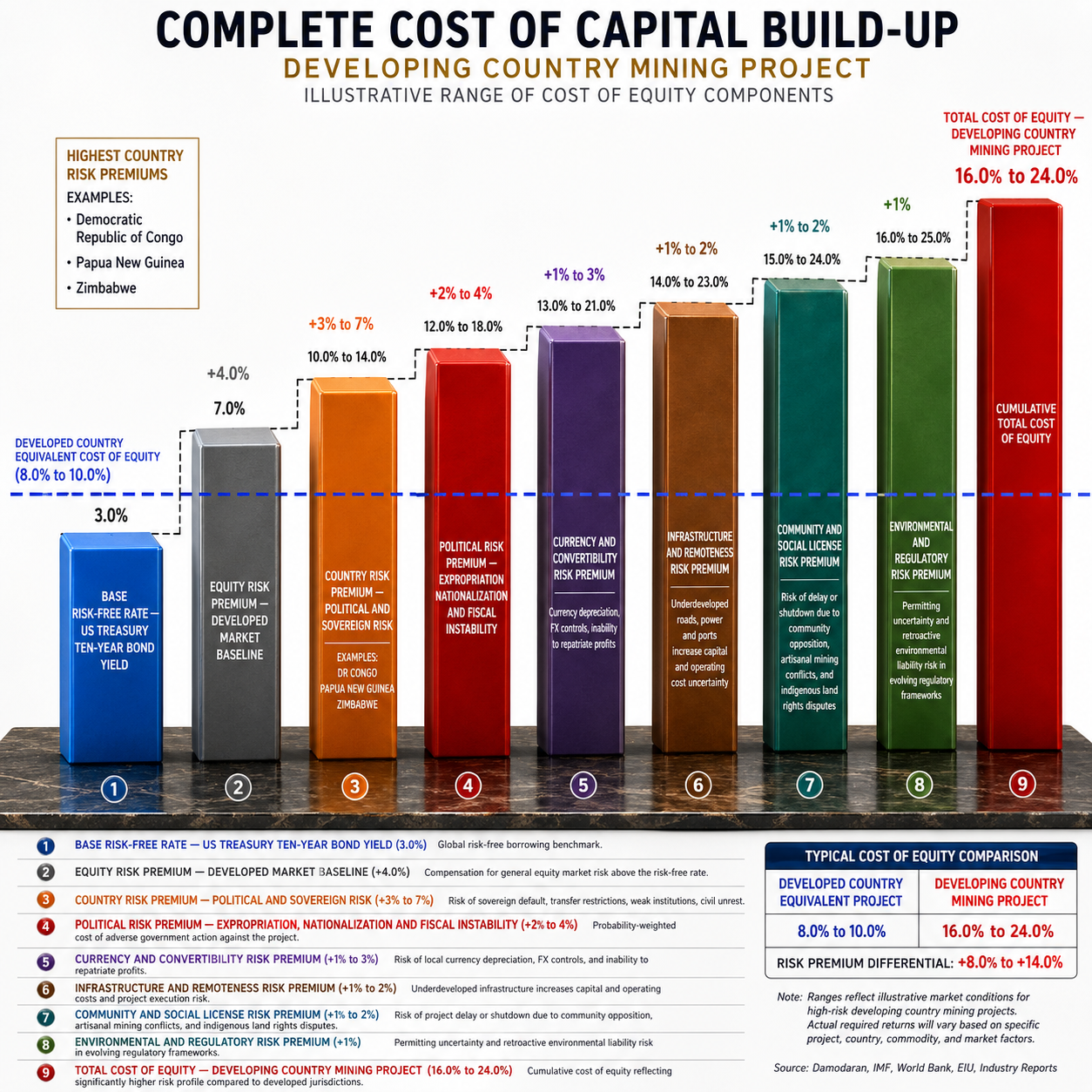

Projects involving mining activities in emerging nations are subject to a series of nonfinancial risks that typically influence the discount rate, interest spread on loans, insurance premiums, and required returns, thereby increasing the cost of capital when such risks are high. These include political instability, policy uncertainty, institutional weakness, lack of infrastructure, foreign exchange and macroeconomic risks, conflict and security risks, environmental and social risks, and challenging financing terms related to commodity price fluctuations.

The most significant cost-of-capital risk factor is the political risk because of fears of expropriation, contract violations, withdrawal of permits, alterations in tax rates, and changes in royalties and ownership policies after investments have been made. As MIGA suggests, political risk in emerging markets for mining ventures is characterized by such factors as revocation of leases or concessions, conflicts with tariffs and regulations, contract violations with governments, and nonfulfillment of obligations by the sovereign.

Uncertainty with regards to regulation and law is also associated with, but not quite the same as, investment risk; however, it requires separate discussion because mining ventures rely on extended approval processes, licensing, favourable fiscal treatment, and enforceable contracts. In its mining sector reforms, the World Bank emphasizes the importance of having a clear, coherent, and enforceable legal and regulatory framework for investments to be easily attracted and sustained. The lack thereof results in increased transaction costs due to uncertain permits and taxes.

Lastly, macroeconomic risk and foreign exchange risk increase the cost of finance by affecting the stability of inflation rates and availability of foreign exchange. MIGA has specifically identified currency inconvertibility and foreign exchange restrictions as insurable risks in the field of mining investment finance. The reason is that an undertaking earning local currency, but servicing dollar debts is exposed to the risk of devaluation, which makes lenders less willing to lend money.

Infrastructure deficiencies represent another major reason behind increased costs due to the fact that there is a high likelihood that the mine will be situated in a remote area where the lack of infrastructure is common. This includes roads, railway tracks, port facilities, electrical power sources, water facilities, and communication networks. According to MIGA, such sites contribute to increased costs and added risk, while the projects will have to invest in the construction of their own road, power, and water infrastructure before they can start production. As noted by the World Bank, deficient infrastructure, skills, and services discourage mining investments, hence requiring higher rates of return from investors.

Security risk and civil unrest increase the cost of mining projects by posing threats to people, equipment, and ongoing operations. MIGA mentions wars, civil disturbance, acts of terrorism and sabotage, and abandonment as some of the dangers facing mining operations that demand investor coverages.

Risks related to the social and environment aspects become more significant as mining ventures require a license to operate from communities, governments, and international financiers. According to MIGA, both types of risks are very significant, and a robust environmental and social program reduces reputational and social risks. If a mining venture suffers protests, lawsuits, resettlement, biodiversity issues, water concerns, etc., additional time for revision and reworking may increase financial requirements and postpone revenue flows. Therefore, the project would incur a higher cost of capital.

Poor governance and corruption negatively impact financing needs indirectly. The World Bank argues that poor governance and institutional quality undermine exploration and exploitation in the sector. In addition, PPP literature on infrastructure development indicates that the environment characterized by the crisis entails various risks including delays, corruption, and ineffective implementation of contracts and plans. Such risks have to be taken into consideration during investments.

Price volatility is one type of commercial risk, but within the mining sector in developing countries, it tends to overlap with country risk and leads to higher funding costs. Price risk causes the financier to be concerned about debt coverage ratios, especially during construction or ramp-up stages, where the miner might find it difficult to raise funds due to lack of resources. That is why high-country risk implies expensive equity or highly-covenanted loans.

Technical risk, which includes operational risks associated with a project, is also important since increased complexity, depth, and lower grades lead to overruns and poor performance. According to EY, operational complexity, variability, and lower grades increase pressure on productivity and cost. At the same time, according to KPMG, macroeconomic risks and supply chain disruptions are among the key industry risks. The technical risks are even more pronounced in developing countries if the local environment lacks qualified contractors, energy sources, skilled labor, and good logistics.

In summary, the key determinants of cost of capital include political and regulatory risks, poor institutional quality, lack of adequate infrastructure, foreign exchange rate instability, security risks, ESG-related issues, commodity price volatility, and complex operations. In practice, this means that there will be demands for higher returns, shorter maturity periods and increased spreads by lenders, and insurance/guarantees provided by institutions like MIGA to bankable projects.