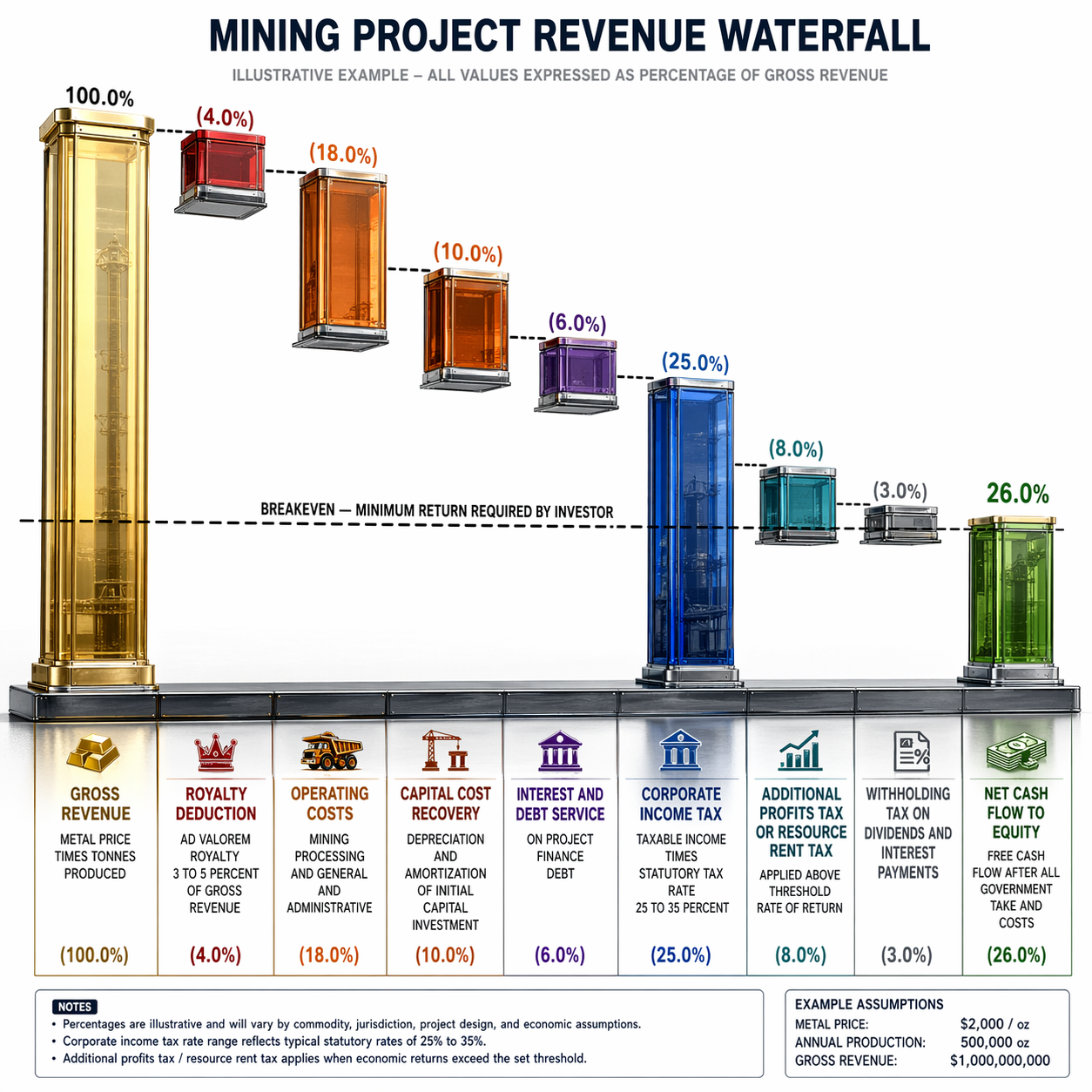

Royalty structures and tax regimes directly shape a mining project’s cash flow, investment attractiveness, and life-of-mine economics. In simple terms, they determine how much revenue the project keeps after the state and resource owner take their share, which then affects NPV, IRR, payback period, and the cut-off grade used to mine ore (Otto et al., 2006; Lilford et al., 2017).

Royalty structures

Royalties are usually paid on gross revenue or on profit. Gross-revenue royalties are easier to administer, but they can be harsh on marginal projects because they are payable even when costs rise or prices fall (Otto et al., 2006). Profit-based royalties are more flexible because they respond to profitability, but they are harder to define, audit, and manage because deductions, depreciation, and allowable costs must be specified clearly (Otto et al., 2006). As a result, royalty design can either accelerate project closure or help a mine remain viable through weak market conditions.

Tax regimes and returns

Mining tax regimes usually combine corporate income tax, withholding tax, customs duties, and royalties. This combined burden reduces after-tax cash flow and can delay the point at which investors recover their capital (Boadway & Keen, 2010). A higher government take may improve public revenue, but it can also lower exploration spending and make investors prefer jurisdictions with more stable and predictable fiscal rules (Otto et al., 2006). Profit-based systems are generally less distortive than ad valorem royalties, yet they still reduce project value because they claim part of the economic rent that would otherwise accrue to the investor (Boadway & Keen, 2010).

Investment implications

The fiscal regime influences how investors rank projects. When royalties are high, low-grade deposits may become uneconomic, pushing firms to raise cut-off grades and mine only the richest ore first (Lilford et al., 2017). That can shorten mine life and reduce total output. By contrast, a well-balanced regime can preserve incentives while still delivering a fair public share of mineral wealth. Predictability also matters: investors often value stable, transparent rules more than nominally low taxes that can change suddenly.

Conclusion

Overall, royalty structures and tax regimes affect not only the amount of profit a mining project earns, but also whether the project proceeds at all. The best fiscal systems are those that raise public revenue without unduly distorting investment, production, and mine-life decisions (Otto et al., 2006; Boadway & Keen, 2010).

References

Boadway, R., & Keen, M. (2010). Theoretical perspectives on mining taxation. In J. Otto, C. Andrews, F. Cawood, M. Doggett, P. Guj, F. Stermole, & J. von Ploennies (Eds.), Mining royalties: A global study of their impact on investors, government, and civil society. World Bank.

Lilford, E., et al. (2017). Quantitative impacts of royalties on mineral projects. Resources Policy.

Otto, J., Andrews, C., Cawood, F., Doggett, M., Guj, P., Stermole, F., & von Ploennies, J. (2006). Mining royalties: A global study of their impact on investors, government, and civil society. World Bank.