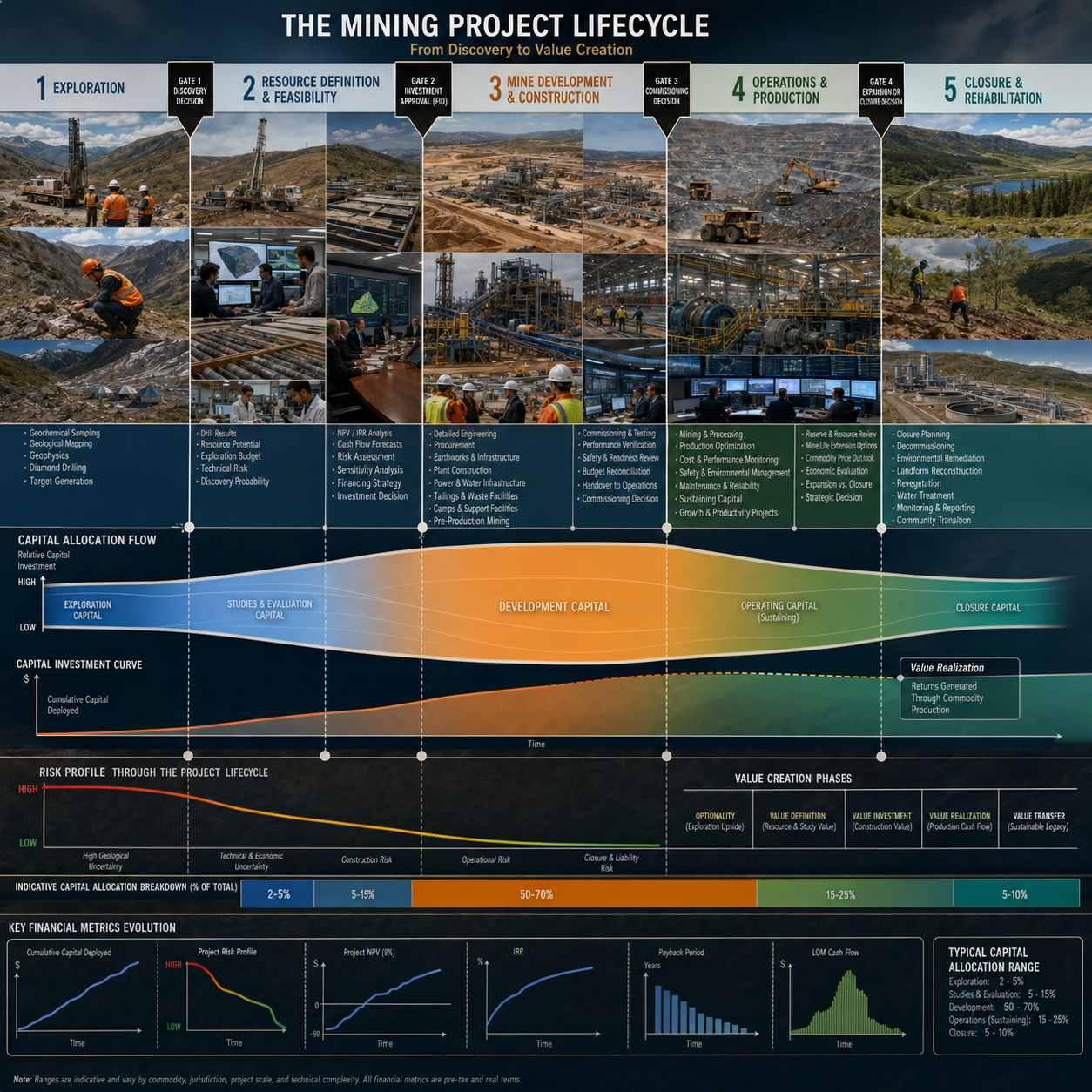

The five key stages of the mining project lifecycle include exploration (mineral deposits discovery and definition), planning and evaluation (feasibility study and permitting), construction (infrastructure development), production (extraction and processing of minerals), and closure/rehabilitation (mine site restoration), while capital allocation deals with how mining companies allocate funding between different projects, and phase gates involve critical management decision-making processes based on the review of certain project-related information to continue with, hold, or abandon the project to save capital expenditure.

In exploration, capital allocation is limited and takes the form of tranches that target acquiring geological information. It involves the expenditures for drilling, sampling, and geophysical surveying aimed at converting geological uncertainty into resource estimation, and the decision-making gates depend on whether there is a sufficient level of estimated resources to conduct a scoping study of the project. As pointed out by Paul Lemmon, a sound operator allocates capital in tranches associated with certain milestone achievement goals (e.g., resource estimation).

The planning/evaluation phase gates (scoping → pre-feasibility → feasibility) see capital expenditures balloon as the estimate accuracy increases from ±50% to ±15%. The scoping study gate answers “What could this project be?” and filters out fatal flaws, the pre-feasibility gate addresses “What should it be?” and develops preferred options at a budget-level capital expenditure, and the feasibility gate seeks to answer “What will it be?” and deliver bankable quotations and reserves necessary for the final investment decision (FID). Risk assessment at each stage justifies proceeding to more costly studies to make decisions, while poor earlier studies are a leading factor behind capital blowouts.

Construction is by far the most capital-intensive phase (accounting for 60-80% of overall CAPEX for the project), while entry into this phase – the FID – requires a bankable feasibility study, funding in place, permits, and quotations for fixed equipment. With an FID in place, capital management becomes focused on execution: financing acquisition, civil works, and commissioning, keeping an eye on the variances in cost. As ATLANTech notes, pre-construction planning is cheap compared to rectifying mistakes, and rapid development saves time before collecting revenues.

In the production phase, there will be changes to the allocation of capital to sustaining CAPEX, growth CAPEX, and exploration for mine extensions. In recent times, the mining industry has been allocating more funds for exploration near the minesite and less funds for grassroots exploration since there is a need for ensuring resource security first before discovery of new mineral deposits under financing challenges. In the gates at the production phase, one needs to consider production effectiveness, cost curve analysis, and investment in growth or divestiture.

The allocation of capital in the closure phase requires that the funding be channeled towards reclamation, water treatment, and post-mining monitoring as indicated in the closure plan incorporated in the earlier phases. RCF explains that there is need for making closure plans as soon as possible to avoid leaving a negative legacy, with the cost estimate being incorporated into operations according to a post-closure vision. The gate into closure will be triggered by orebody exhaustion or grade degradation with funding allocated for land restoration.